Topping last year’s record numbers, European components distribution ended the first quarter of 2023 with surprisingly strong sales numbers for both Semiconductors and IP&E; (Interconnect, Passive and Electromechanical) components. Semiconductors in Q1 2023 grew by 22,9% to €4,08 billion, IP&E; by a much more moderate 0,9% to €1.82 billion. Q1 in total grew by 15,2% to €5.9 billion.

Hermann Reiter, chairman of DMASS: “After Q4 of 2022 it was hard to imagine that our market would grow again, both year on year and sequentially, specifically since the slowdown in orders was visible for a few months now. The surprising revenue growth in Q1 cannot hide the reality of rather full inventories in the channel. At the same time, we share the general optimism in the European industry that the slowdown will be short. As our core business segments aren’t PCs and smart phones, but thriving segment like automotive and industrial, we are confident that after the inventory digest, demand will grow again dynamically.”

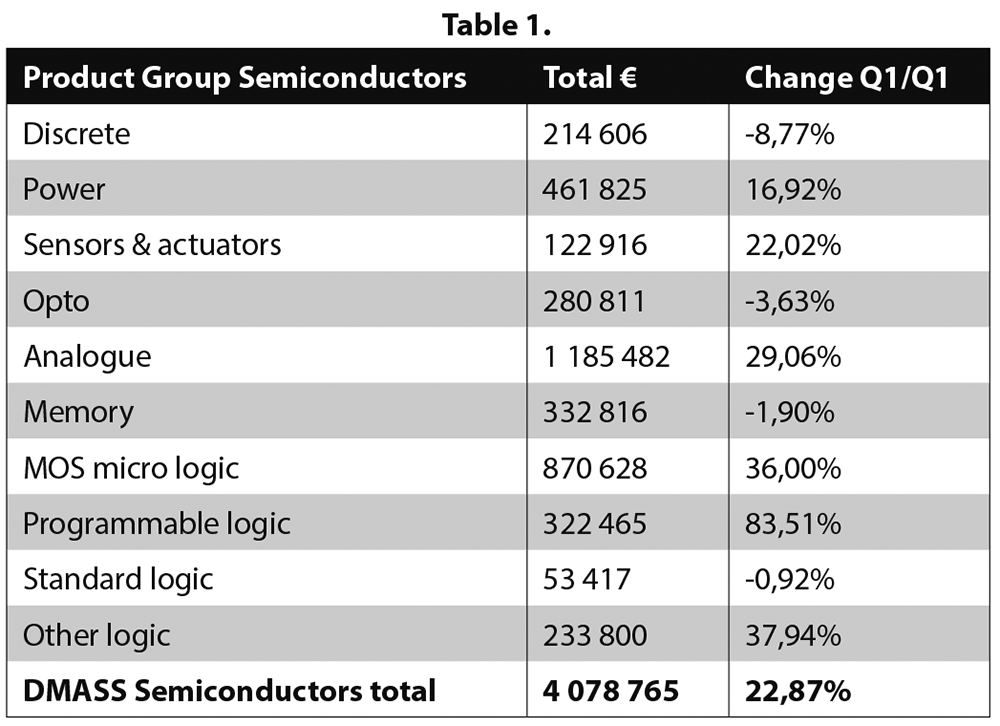

Semiconductors

With a total of €4,08 billion, DMASS delivered the highest ever reported semiconductor revenues. The growth occurred across all countries and regions, although in varying pace. Of the major countries, Germany recorded the highest increase. Product-wise, micros, programmable logic, and other logic (ASICs, ASSPs) showed the highest growth, followed by analogue products (see table 1.).

Interconnect, passive and electromechanical components

The IP&E; segment showed a surprising sequential uptick of 15% versus Q4 2022, but a tiny growth of 0,9% to €1,82 billion versus Q1 2022. Growth distribution across countries was totally different from semiconductors (which is mainly due to a different membership structure in IP&E). While passives decreased by 2,3% (special passive components saw an increase), connectors and electromechanical components, and power supplies remained positive (see table 2).

Reiter said: “The growth curves in semiconductors and IP&E; have been quite different for a while, with IP&E; growth peaking a few quarters before semis. Therefore, we have been positively surprised in Q1. What is also visible is that special components on both sides are still seeing growth peaks which may indicate a shift away from standard technologies.”

However, the special situation in distribution, compared to a total market that sees stronger skid marks, makes a prediction difficult, said Reiter: “Bookings have certainly decreased, but not to the extent we have feared. We would expect a slowdown for 2023, but at moderate levels, and see a lot of optimism from customers for the long-term prospects of the components business in Europe.”

© Technews Publishing (Pty) Ltd | All Rights Reserved

printer friendly version

printer friendly version