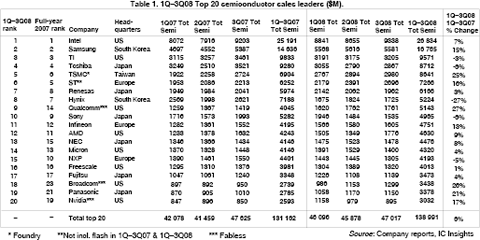

IC Insights’ recent research for its November update to the McClean report includes an analysis of the top 20 semiconductor suppliers for the first three quarters of 2008. There are eight US companies in the top 20 (including three fabless semiconductor suppliers), six Japanese, three European, two South Korean, and one Taiwanese company (IC foundry supplier TSMC) in the ranking.

As shown in Table 1, it required at least $3,0 billion in 1Q-3Q08 sales to make the top 20 ranking. Although the top four ranked companies remained the same, and most of the other top 20 suppliers moved up or down only one or two spots in the ranking, there were a few companies that displayed significant changes in their 1Q-3Q08 ranking as compared to their full-year 2007 positions.

Major changes in the ranking include:

* Cellphone IC supplier Qualcomm used a 27% year-over-year growth rate to jump five spots and rank as the ninth largest semiconductor supplier through the first three quarters of 2008.

* The third largest fabless supplier, Broadcom, jumped five positions and is now positioned as the 18th largest semiconductor supplier in the world.

* DRAM-supplier Qimonda’s nightmare worsened in 3Q08 as the company dropped 12 positions from being ranked 18th overall in 2007 to 30th in the first three quarters of 2008.

* With a 5% decline in 1Q-3Q08/1Q-3Q07 sales, NXP fell five spots to 15th from 10th in 2007. For all of 2008, the company’s sales are forecast to decline 11% as compared to 2007.

Summary

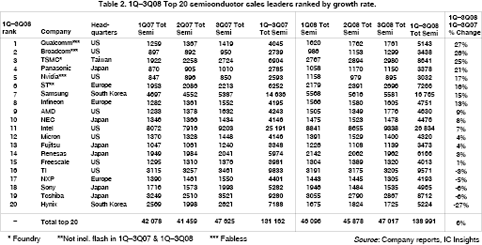

With some major DRAM and flash suppliers (eg, Qimonda, Elpida, and Spansion) no longer part of the top 20 ranking, the total 1Q-3Q08/1Q-3Q07 sales of the top 20 semiconductor suppliers displayed a relatively strong 6% increase as compared to the total worldwide semiconductor market increase of 4%. Among the top 20 semiconductor suppliers, there was a 54-point swing (Table 2) from the company that showed the fastest growth (Qualcomm at +27%) to the company that registered the steepest decline (Hynix at -27%).

As shown in Table 2, eight of the top 20 companies had double-digit 1Q-3Q08/1Q-3Q07 growth rates. Moreover, all of these companies registered 1Q-3Q08 growth rates that were more than three times the 4% growth rate of the entire 1Q-3Q08 semiconductor market. It goes to show that there are still strong performers in a slow market.

Given the current state of the worldwide economy and the weakening semiconductor markets, IC Insights expects that the top 20 semiconductor suppliers, in total, will register 4Q08 sales of $43,2 billion, a decline of 8% sequentially. It should be noted that the star growth company in the first three quarters of 2008, Qualcomm, has warned that its calendar year 4Q08/3Q08 sales are expected to drop about 28%. However, its current full-year 2009 WCDMA/CDMA cellular phone device shipment forecast is +25%, essentially the same growth expected for 2008.

For full-year 2008, the top 20 semiconductor suppliers are forecast to have combined sales of $182,2 billion, a 2% increase over 2007. This 2% increase is the same growth rate expected for the 2008/2007 worldwide semiconductor market.

For more information visit www.icinsights.com

© Technews Publishing (Pty) Ltd | All Rights Reserved

printer friendly version

printer friendly version