Fixed wireless access (FWA) is bridging the digital divide, by connecting millions of previously unconnected people each month.

Territories where access to connectivity has been challenging, such as rural communities in the US or the Empty Quarter in Saudi Arabia, can now be profitably served with connectivity via FWA. Lower GDP nations, which have not been able to justify 5G investment, can be served with 4G/LTE FWA, which offers usable internet speeds but uses cheaper chipsets and network infrastructure than 5G. 4G can deliver peak speeds of 100 Mbps, and mobile operators claim typical download speeds of 50 Mbps or more. Importantly, 5 Mbps is easily sufficient for streaming video, while 4K ultra-HD video needs at least 15 Mbps.

The arrival of 5G has made FWA even more attractive to people because of the low latency and high throughput it delivers – and 5G-Advanced will further this appeal. Speeds can be lightning fast, with one operator in Japan claiming a highest speed of more than 350 Mbps in some areas. However, with some 5G FWA customer premise equipment (CPE) still in the $500-700 range, cost has been well above the level that the mass-market will accept. The Japanese operator, for example, used high-performance CPE to enlarge cell capacity, but this made its deployment more expensive. Ultimately such costs end up being paid for by customers, so business cases must be carefully assessed to gauge affordability.

The need for speed

The theoretical maximum speed for 5G is approximately 1 Gbps, but given the shared nature of networks, it is unlikely that consumers will see this often – although speeds are sure to rise from the current averages as enhancements arrive. 5G-Advanced may change the picture even further with its theoretical maximum speed of 8 Gbps. However, this remains a distant prospect for most users. Yet FWA provides an experience that is at least comparable to fixed broadband offerings where available and, of course, is the only alternative to satellite in areas with no cabling infrastructure.

A significant bottleneck is the cost of equipment, which needs to further reduce to open up the global mass market. This will be achieved as supply chain issues are resolved and greater volumes drive cost savings. If the economics can be made to work for the mass market, 5G FWA will become an even more exciting opportunity for service providers, because it provides a means to monetise their network investments in 5G, and in some markets there’s the possibility of accessing government funding to connect citizens.

Preserve affordability

Network infrastructure and CPE costs, however, remain an issue for many 5G FWA business models, so LTE FWA continues to be rolled out to address the needs of users in many markets that cannot sustain a 5G business case.

Often, these deployments bring internet connectivity to users for the first time. With 4G and 5G FWA, users that will never be served by fibre, because of low population density or challenging levels of disposable income, can connect, taking advantage of the cost-effective deployment characteristics of the technology.

A critical enabler in these markets is affordable CPE, such as low-cost 4G and 5G FWA hubs, and the availability of modules for PCs and other devices that can connect using Wi-Fi or cellular technologies.

Market landscape

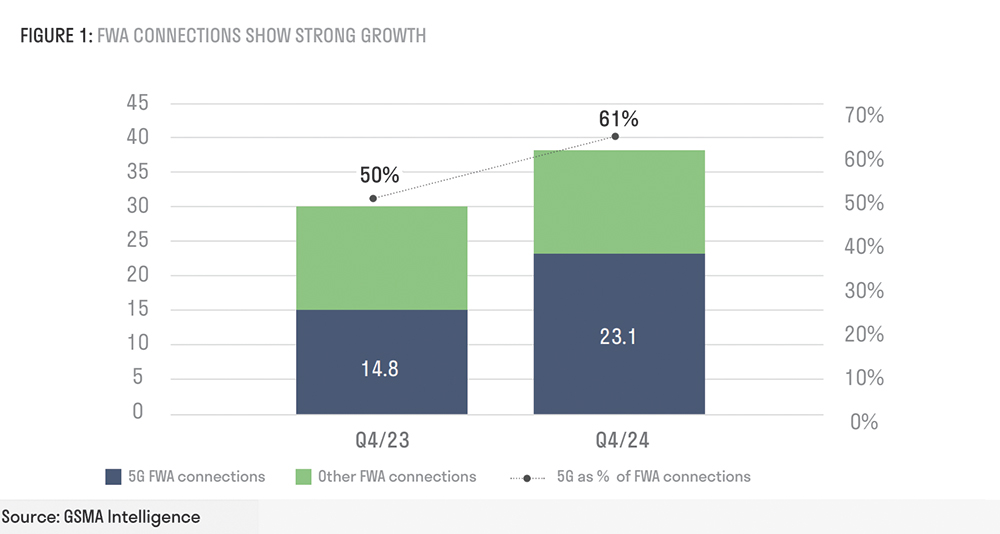

FWA has gained significant momentum as a flagship 5G use case, and markets across the globe are adopting the technology to connect the unconnected. GSMA Intelligence predicts breakout growth of 55% for 5G FWA in 2024, with 5G accounting for 61% of FWA connections in Q4 2024.

Meanwhile, research firm Dell’Oro Group has released figures that suggest total FWA revenues, including radio access network (RAN) equipment, residential CPE, and enterprise router and gateway revenue remained on track to have advanced 27% in 2023, driven largely by residential subscriber growth in North America, and growing branch office connectivity deployments globally.

The firm projects that global FWA revenues will exceed US$9 billion by 2027, with long-term subscriber growth expected in Southeast Asia and the Middle East and Africa. Part of this will be driven by network upgrades from 3G to 4G and the firm projects global spend on FWA access equipment will pass US$40 billion over the next five years, with spending on 4G and 5G-enabled enterprise routers and gateways set to grow by US$4 billion by 2027.

Others are more bullish. Counterpoint Research has projected a cumulative US$200 billlion global FWA CPE market in the period 2022-2030. By 2030, the firm estimates that global FWA subscribers will exceed 462 million. 5G FWA traffic will hit 574 exabytes in 2030, up from 5 exabytes in 2022, while 5G FWA subscribers will grow at a CAGR of 54% between 2022 and 2030.

For further reading, visit https://bit.ly/3Qfh992

| Email: | [email protected] |

| www: | www.quectel.com |

| Articles: | More information and articles about Quectel Wireless Solutions |

© Technews Publishing (Pty) Ltd | All Rights Reserved

printer friendly version

printer friendly version